Selecting a therapist can feel like a daunting task. You’ve probably thought about location, specialty, training, and the cultural background of the therapist,. And of course, another important question you’ve likely wondered–what’s the cost of a session? Many clients will look for a therapist who is in-network with their insurance to make services more affordable. However, in many cases, your preferred provider may not accept insurance at all. This is often true for specialized therapy, like couples counseling, or for private practice owners who choose to limit the administrative overhead by sticking with out of pocket pay only.

Fortunately, insurance companies often provide reimbursement for out-of-network (OON) professional services, including therapy, which can help reduce costs considerably. Before deciding that your preferred therapist is too expensive, you can check with your insurance company to see what percentage of the fee they will reimburse. The insurance company will need a few things from you in order to make that decision including a superbill.

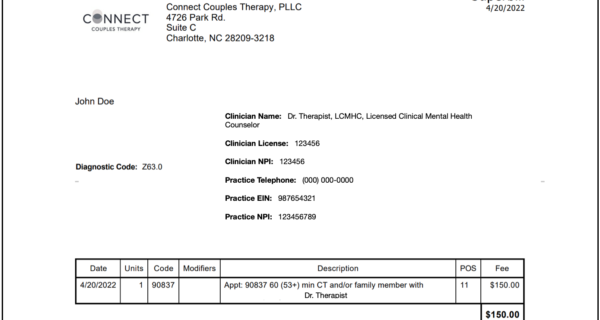

What is a superbill?

A superbill is a detailed receipt of the services you have received. A superbill lists the sessions you received, and includes procedure codes, diagnosis codes, and therapist and practice information. Typically, the client submits the receipt directly to their insurance carrier, giving the insurer all the information required to be reimbursed for their claim.

How much could be reimbursed with a superbill?

After you meet your deductible, many plans will cover a percentage of OON services. It is important to note, however, that only some clients will receive reimbursement, and that insurance companies rarely offer full reimbursement for the fees associated with therapy. A superbill does not guarantee reimbursement, but is necessary for determining what you might be eligible to receive. Finally, be aware that if you have a high deductible, your insurance company’s rates of reimbursement may not immediately make therapy more affordable; for example, you may not meet your deductible before your yearly policy renews, and thus would not be eligible to receive any reimbursement.

In order to avoid surprise costs, call your insurance company ahead of time to determine what they will cover.

3 steps to request and use a superbill for therapy cost reimbursement

- Ask your therapist if they can provide a superbill, either prior to starting therapy, or after your first session. Don’t feel awkward asking, as this is a common request. If your therapist is unfamiliar with superbills, ask if they would be willing to learn how to create one–there are a number of free templates available online. If you have concerns about receiving a diagnosis (which insurance companies typically require), make sure to address this with your therapist beforehand. You can ask your therapist to clarify which diagnosis they intend to submit, their reasoning for making that diagnosis, and what the implications might be as a result of adding that diagnosis to your medical record. If you feel uncomfortable with your therapist’s proposed diagnosis, ask about possible alternatives.

- Speak with a representative from your insurance company prior to starting therapy, or submit a claim to your insurance after starting therapy. If you want to determine what your insurance will reimburse ahead of starting therapy, simply call your customer care number (on the back of your insurance card), and ask a representative to calculate the reimbursement rate. Otherwise, after your first therapy session, submit a claim to your insurance company. Most companies provide an online portal in which you can upload specific claims forms, as well as your superbill. It may take a few weeks, but you will receive an Explanation of Benefits (EOB), showing your rate of reimbursement.

- Continue to upload claim forms and superbills for reimbursement, as you progress in therapy. Some insurance companies and policies will allow a certain number of visits to be listed on each claim form (e.g., no more than ten), which means you may not need to submit a new claim after each therapy visit. Clarify this with your insurance representative beforehand.

If you are considering starting therapy with an out-of-network provider, the superbill is a useful tool that might make your services more affordable. Check with your therapist to see if they can provide a superbill, and guide you through the necessary steps to submitting one. Be sure to address any lingering questions or concerns ahead of time.

Need a bit more help?

If you are ready to schedule an appointment and live in Arizona, North Carolina, South Carolina, or Texas, we can help. Contact us to get started. We offer virtual and in-person sessions, and superbills, upon request.